Building a personal budget sound incredibly boring, doesn’t it? I’m here to tell you that they aren’t. They are actually really important for your day-to-day success. Why do you think larger companies have a corporate budget? They need to know what they are spending money on, of course. Comparatively, you need a personal budget as a tool to help ensure your success.

In this article I give five easy steps to create a personal budget and tips to consistently use it. Finally, I will give you my personal thoughts on budgeting for your future. It is important to discuss what a budget can do for you.

What a Personal Budget does for you

Some of you may know that I like to define my terms whenever I start a new post, so in like manner, we should define what a budget is. Investopedia defines a budget as an estimation of revenue and expenses over a certain period of time in the future. Basically, a budget lets you see how much money is coming in versus how much money is going out. There are three types of budget outcomes: a surplus budget, deficit budget and a balanced budget. For a personal budget plan, it’s preferred to have a surplus or balanced budget. In short, you have either paid off all your expenses and have no debt (balanced) or you have paid off all your expenses and have extra money left over (surplus). Balanced is good, but we like having extra money left over!

More specifically, a personal budget helps you understand where you are spending your money and if you need to make changes to your spending habits. Have you ever come to the end of a month and think, “where did I spend all my money?” That’s probably because you don’t track your spending. A personal budget would help you monitor this and be able to save or invest in your future. More on savings and investing in my Tips for Saving and Investing post.

How to build a Personal Budget in 5 steps

If you build a personal budget, I guarantee it will be beneficial in many ways beyond just knowing what you spend. You may ask, how to build one? Below are 5 easy steps to do this. Best of all, if you have any spreadsheet software or a smart phone of any kind, you can do this quite easily.

Check your Financial Information

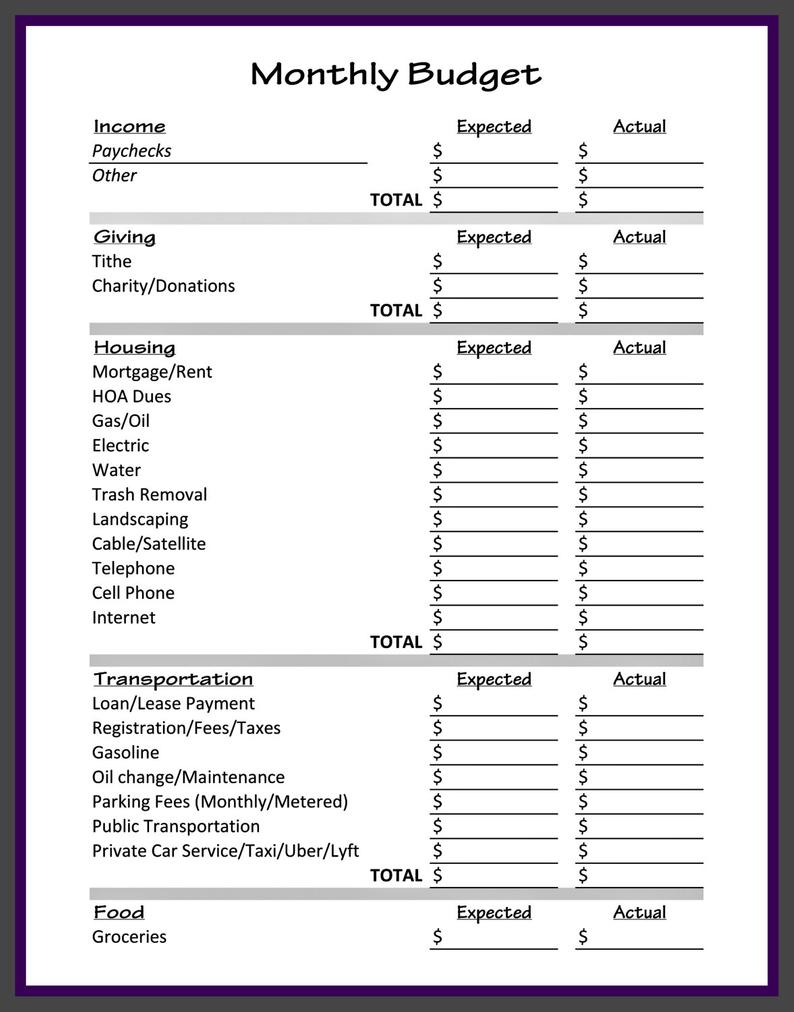

- Take inventory of your financial situation. This is the most important part of the process and key to your personal success in creating a budget. To take inventory of your finances, you must gather all your financial information.

- Review bank statements, investment accounts, credit cards, loans, utility bill, pay stubs, receipts from the last few months, etc.

Your Income Matters

- Start with those paychecks. We want to take a look at any monetary source. This doesn’t just mean paychecks; if you have a side business that you get 1099’s from, add that in.

- If you have a consistent interest payment from an investment, include that as well.

- Basically, we are looking for anything that pays you something.

Expenses are Key

- Watch for planned and predicted expenses. This section is called the “expense” section. This step could be the most intensive depending on your lifestyle.

- Once we have established the monthly income from the previous step, we need to compile the expenses. In this step, we need to create expense accounts to add to our budget. These items need to be separate line items on your budget.

- Add lines for mortgage or rent, car payment, utilities and cable/internet, groceries, going out, clothing, gym fees, etc. If you are putting money away or investing every month, that should also be a line item. To be honest, anything that you spend money on should be considered an expense and needs to be added.

- The most important part in this section is to be completely honest with yourself. If you don’t consider all your expenses, you will only hurt yourself in the end.

Cash Flow

- Compare what you take in versus what you spend, and adjust. This is the cash flow analysis section and the part that may or may not require some math skill.

- Add up all the expenses and subtract them from the revenue section and what you have left over is your surplus or deficit. If you were honest in step three and have a positive balance, that is great news! If you have a negative number in this section, then it could be time to rethink the expense section. This is where the adjustment process can come into play.

- If you found some expenses that maybe you don’t need, (i.e., cable subscription that you don’t use or a dating app that you haven’t looked at in years but still paying for), cancel it.

- There is no need to pay for something you don’t need or use. This is the power of having a budget. Now you know!

Control the Spending

- Establish boundaries for your spending. If you are brand new to creating a budget, then you may not understand how much is “correct” to spend on each account. The general rule is that you want to have a surplus left over as a buffer. However, if you also invest or save, include that in the monthly budget. Maybe your budget is balanced instead of in surplus.

- Generally, housing cost should not exceed a max of 30 percent of your gross income per month. I would honestly suggest spend closer to 15 percent of your gross income on housing cost per month and use the remainder to invest in yourself.

- Any other costs need to be evaluated based upon your analysis from the first step. If you spend 500 dollars per month on groceries, but 1000 dollars per month on going out, maybe you go out too much. But again, this is all relative and will depend on your income. By establishing budgeting boundaries, you can see where you are and where you can revise when needed.

How to stick to your Personal Budget

Now that we know the basics on how to create a budget, let’s discuss how to stick to the budget. Sticking to a budget can be harder than creating the budget itself. There are so many distractions and enticements to spend money frivolously. The best way to stick to a budget, in my opinion, is to think of the main purpose of the budget. What is your main purpose? Are you worried if you have enough money? Are you curious if you can afford something?

Understand your goals and think of that whenever you make a purchase. I cannot tell you how many times I have mulled over a purchase and in my mind I’ve said, “do I really need this?” We are a very consumption-based society and our society says, “if you want it, buy it.” This is not the best way to live life and it certainly doesn’t help to easily and consistently maintain a personal budget.

Envelope System

Another way to stick to a budget that requires less self-control is going to a cash-based system. Oftentimes, it is harder to spend actual cash than just swiping your debit card. Therefore, many people I know that watch their spending have switched to a cash only basis. In this scenario, you only have an ATM card and must pull out cash whenever you need to make a purchase. This is known as the “envelope system”. Cash is divided into separate envelopes with the corresponding expense written on the outside. When the cash is spent, no more purchases are made for that expense. It can be very effective on controlling your spending.

Myths on Needing a Personal Budget

I hear many people say, “I don’t need a budget,” or “budgets are hard.” In this section, I want to expel some myths that you may have heard about creating a personal budget. Budgets are for everyone, whether you are rich, broke, or in the middle. It does not matter. A budget helps you understand your financial snapshot. It helps you understand where your money goes. If you don’t know where your money goes, odds are you are overspending. Money is a tool that can be used for many things; use it effectively.

If you think budgets are hard because you “aren’t good at math,” or you “aren’t disciplined enough,” I have good news. There are apps that can do it for you. Here are the 7 best Budget Apps for 2021. Budgets do not have to be hard. If you think they are hard because you don’t want to think about how much money you spend, maybe there is a self-control issue there. It’s important to think about the future. If you are living under the notion that you want to spend everything on entertainment and pleasure, understand that those things are temporary. You may never be able to stop working in order to pay for your lifestyle.

My Thoughts on a Personal Budget

I use and check my budget daily. I’m actually a little old school in the sense that I use Excel for my personal budget. I just prefer to be more involved in the number crunching. The budget apps are very easy to use and work well. I just prefer to do it more myself. A budget helps me understand what money goes in and what money goes out. I also have a personal business that I use a budget to track all of my expenses and revenue.

One key account that everyone should have as a line item on their personal budget is investing in yourself. I don’t mean buying the best watch, purse, or the newest shoes on the market. I mean investing in your personal development. If you have any desire to grow your income through a second job or a side hustle (which, by the way, you should!), you must invest in your own knowledge.

I buy programs and read books on investing in real estate, stock market and e-commerce quite frequently. For more on building a business, read my post on The Mindset of an Entrepreneur. The business world changes so rapidly that you need to stay on top of all the new programs and options that are out there. A last benefit of budgeting allows you to know how much you can spend on personal investment.

Disclaimer: I receive affiliate compensation for some of the links in this article at no cost to you. However, these are the best tools I have used and tested that I believe are most effective for launching and running an online business. You can read our full affiliate disclosure in our privacy policy.

Before you go…

Do you want to learn how you can take ANY business and scale it to achieve your dreams and goals?

Partner up with me by clicking on this link and watching the video.

We will show you EXACTLY how to build a business online and customize a plan just for you. We will help you choose a niche, setup your online business and help with selecting offers that you can promote.

On top of that you will get ONE on ONE mentoring to make sure you are doing things right.

A great way to be able to save more money is when we make more money.

Cheers to your success and See you at the Top!

-Cameron